Seller Finance Your Business In 2026

Table Of Contents

Essential Concepts

If you are selling your business or making plans to do so, seller financing is an excellent tool that you should consider utilizing.

Most businesses are small businesses [1] and most small businesses are sold using some amount of seller financing. [2] This approach might not be the goal of business owners, but there is much good advice available that advocates seller financing.

Seller financing also known as owner financing or seller carry back, means that the seller will carry a note, ie. a secured promissory note, and receive periodic payments for at least part of the selling price of a property, business or some other asset. When a business is sold using seller financing, the secured promissory note is known as a business note.

Should you seller finance your business? The advice about seller financing varies depending on the source's point of view. That advice will vary futher depending if it offers a seller's or buyer's perspective. What if you might sell the note or part of it later? This is an important consideration and one often given limited thought.

In this article I will synthesize a number of concepts related to selling a business, while keeping in mind the idea that the seller of the business may benefit by also selling the business note thereafter

When you are ready to sell your note or part of it, as a note broker NoteSolutions will do the work to maximize the value of your note.

It's important to view this process to a certain degree as a financial puzzle, with moving parts. In this puzzle a business seller and advisors are looking for a productive solution that will provide the best combination of sales price and terms, minimize and/or defer taxes, and do so in timely fashion, while finding the right buyer who will operate the business successfully and profitably.

Considering the points above, you need to make a decision that seller financing will work for you. Read on and hopefully this approach wll work for you based on your circumstances.

Advantages For Business Sellers

By using seller financing to sell your business you will exert a greater degree of control over the marketing, financing and sales process. Once you've decided to provide seller financing, you can move this process in ways that will achieve the specific results you desire.

For tax purposes, seller financing is referred to as an Installment Sale. This allows you to pay taxes on your profit as you receive it, which is spread out over time. An installment sale can be used in conjunction with a 1031 Tax Deferred Exchange for additional tax benefits. I will discuss these points further below.

Seller financing can be combined with other financial resources to purchase your business. Depending on your personal situation, you can select the amount of financing you prefer to offer.

In order to create a sellable business note, the buyer of your business should make a cash down payment of at least 20%, while 30% is prefered by many business note buyers. By offering up to 80% seller financing, you put yourself in position to maximize the tax benefits as well as other benefits.

As other business sellers are reluctant to provide seller financing, or only will offer a small amount, you will access a much larger group of potential buyers by providing more financing. By offering terms instead of requiring a lump sum payment, you should receive a higher price for your business. And you will collect interest on the monthly payments. You will also close faster without a bank involved.

The ideal candidate to purchase your business and operate it moving forward, may not be able to obtain the financing that you find ideal, or that your advisors think is best. So if you are still on the fence about providing seller financing, the biggest benefit of doing so could be getting the buyer!

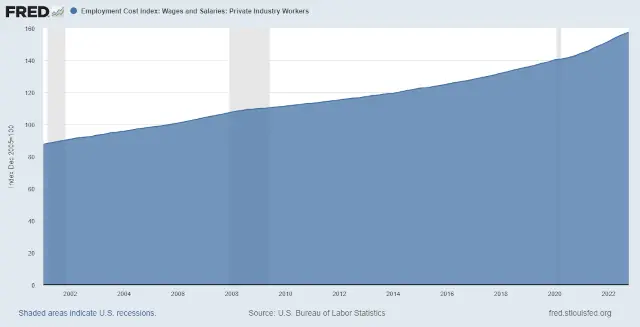

U.S. Bureau of Labor Statistics, Employment Cost Index: Wages and Salaries: Private Industry Workers [ECIWAG], retrieved from FRED, Federal Reserve Bank of St. Louis, March 2, 2023.

"The Employment Cost Index, or ECI, measures changes in the cost of employees to employers over time. In the private sector, business owners and human resources professionals can use the ECI to make decisions about pay adjustments to help them stay competitive. In the public sector, the Federal Reserve and others use the ECI to gauge the health of the labor market, adjust contracts, and research the labor market."

In the graph above the Employment Cost Index increased from 87.6 in the first quarter of 2001, to 157.5 in the fourth quarter of 2022.

Advantages For Business Buyers

Financing to purchase a business can be difficult to obtain, especially from a bank. Being offered seller financing makes life that much easier for the business buyer. While business sellers must do proper due diligence, they don't face restrictive institutional guidelines.

Creativity in structuring the business note is beneficial to both the business seller and the business buyer. By determining the needs and capabilities of both buyer and seller, seller financing is a tool that provides flexibility to structure a win-win deal.

Seller financing gives the buyer the opportunity to reduce purchase costs. Of course this will vary depending on the buyer. For buyers able to qualify for premium institutional financing or low cost friends and family financing, this may not apply. Most business buyers are not in such a favorable position. So their alternatives become more costly.

By comparison, with seller financing the business seller can attain a higher price while it's still affordable for the buyer. To the extent that bank financing is reduced or eliminated, buyer closing costs are reduced. Lender closing costs may include an origination fee, loan packaging fee, tax monitoring fees, flood certification and SBA guarantee fee. Other fees may apply to both seller financing and bank financing.

There are also socioeconomic advantages that benefit both the buyer and the seller. Institutional financing comes from a source outside the transaction, based on profit motives. Seller financing brings together the two parties most interested in making a deal. Each of these parties may have strengths and weaknesses that they can work through with greater incentive than a bank will have.

While a bank may see a potential business buyer that doesn't meet the requirements of a specific financing program, the business seller may see a potential buyer well suited to be the next person running their business.

The business seller can evaluate all pertinent aspects of the buyer, and develop confidence that the business will succeed after the sale. While economic factors may be changing, seller financing is a way to share this confidence in the ongoing success of the business with the buyer. So let's find a way to make this work!

Action Step

Business sellers that provide seller financing will have different levels of interest in doing so. Knowing that business notes can be sold offers a way out if you want it. Your view on this may change as you learn more about it, as other options to sell your business may not work as you want, and as your circumstances change after you sell your business.

In order to provide seller financing a promissory note must be written. This will happen somewhat naturally as financial terms of the business sale are agreed upon. As the business seller it's better to know in advance how you want to proceed. Take a look at how a business note buyer would structure a note to maximize the value of your business note.

Installment Sales

Photo by Kelly Sikkema on Unsplash

I mentioned installment sales above as one of the advantages of seller financing. In United States income tax law an installment sale is a sale of property (including businesses), where you will receive at least one payment after the tax year in which the sale occurs.

IRS Topic 705 summarize some of the relevant points. "You are required to report gain on an installment sale under the installment method, unless you "elect out" on or before the due date for filing your return (including extensions) for the year of the sale. You may elect out by reporting all the gain as income in the year of the sale...."

Situations Where The Installment Method Isn't Permitted

"There are some situations where the installment method is not permitted. Installment method rules don't apply to sales that result in a loss. You can not use the installment method to report gain from the sale of depreciable assets that are ordinary income under the depreciation recapture rules in the year of sale."

Determining Your Total Gain

"Your total gain on an installment sale is generally the amount by which the selling price of the property you sold exceeds your adjusted basis in that property. The selling price includes the money and the fair market value of property you received for the sale of the property, any of your selling expenses paid by the buyer, and existing debt encumbering the property that the buyer pays, assumes, or takes subject to."

Reporting Interest

"You generally report interest on an installment sale as ordinary income in the same manner as any other interest income."

Additional Information

To expand on the points above and for additional information refer to IRS Publication 537, Installment Sales.

Key Thoughts On Installment Sales

With proper planning it's possible to minimize or defer some of the taxes you will face by selling your business. Seller financing, through the use of installment sales, gives you one approach that can help with this process. You will want as much of the money you make from the sale to be taxed as capital gains, rather than ordinary income.

The tax rate on long term capital gains ranges from 0 to 20% compared to a maximum ordinary income tax rate of 37%. For more insights take a look at What Are The Tax Implications Of Seller Financing?

Seller Financing And 1031 Exchanges

If you read Make Your Business Note Profitable, you learned that note buyers prefer that when a business is sold, any real estate sold be handled with its own note, separate from the other business assets. This approach works well if you are already planning to do a 1031 Exchange, whether or not you have any plans to sell the business note in the future.

This approach becomes more advantageous now that the Tax Cuts and Jobs Act has restricted 1031 Exchanges to real property.

If you sell real property using seller financing, you have the choice of including or excluding the note from a 1031 Exchange. If you exclude the note from the 1031 Exchange, the comments above regarding installment sales apply. The rules that apply are those of Section 453 of the Internal Revenue Code.

If you include the note in the 1031 Exchange, the rules that apply are those of Section 1031 of the Internal Revenue Code. To learn more about this I suggest you review "Seller Carry Back Notes and 1031 Exchanges."

Is The Potential Buyer Of Your Business Considering An SBA Loan?

If your buyer is able to obtain an SBA loan, this may be the financing with the lowest interest rate, and the longest term that the buyer can find. It also may be difficult to obtain, time consuming and include terms that are not appealing to the seller.

IMPORTANT:

The SBA Standard Operating Procedures (SOP's) are official, legally binding guidelines governing SBA loan programs. Some aspects may stay the same for years. Othes go back and forth between easier and more stringent terms. The SOP effective June 1, 2025 is close to 500 pages long. And there are new updatesin 2026. Without that detail and constant updating, below I am offering information to give you a heads up in key ways.

Here are some points to consider as you evaluate seller financing:

- The SBA does not loan money. They guarantee bank loans up to a certain percentage.

- Many small businesses won't pass the SBA requirements.

- An excerpt from the Electronic Code of Federal Regulations states : "SBA requires the Lender or CDC (Certified Development Company) to certify or otherwise show that the desired credit is unavailable to the applicant on reasonable terms and conditions from non-Federal sources without SBA assistance, taking into consideration factors associated with conventional lending practices..."

- The SBA 7(a) loan is their main program for providing financial assistance to small businesses. Effective January 1, 2018 the SBA made some changes to the rules for this program.

- Banks are now allowed to finance up to 90% of a deal, lowering the equity injection requirement to 10%. Of that at least 5% must come from the borrower. Up to 5% can come from a seller note.

- These are minimum requirements for the SBA to guarantee the loan, and individual banks will have their own requirements.

- If a seller note is used for the equity injection, full standby applies for the life of the loan. This means that no principal or interest will be paid on the seller note for the term of the loan.

- When a bank loan is used to purchase a business, a seller note will be subordinate to the lender, whether or not an SBA guarantee is provided. This means that if the buyer defaults, the bank is in first position for proceeds from the sale of any collateral.

- One suggestion you might receive is to provide a second seller note. This is in addition to the equity injection contribution. The buyer may be able to make payments on this note as soon as the deal closes. But if you ever want to sell this note you will have difficulty doing so. And this note will also be subordinate to the lender.

- In the points above there is a fine distiction between the SBA requirements for a seller note that's part of the equity injection, and an additional seller note subject to individual bank requirements. In the latter, banks may also have standby requirements limiting the seller's ability to collect payments from the borrower (the business buyer) and limit claims against the borrower as well.

- To enforce lender standby requirements SBA Form 155 is used. You may be surprised to see the details.

- The SBA's Standard Operating Procedures effective January 1, 2018 include: "5. If the Borrower will be acquiring the small business’s real estate in a separate transaction with a non-SBA guaranteed loan, the SBA loan must receive a shared lien position (pari passu) on the real estate with the non-SBA guaranteed loan. This provision does not apply if the business real estate is being financed as part of a 504 project."

- So if you take the advice to finance the sale of your real estate using another note separate from the business, and an SBA loan is used to purchase your business by the same buyer, you are still faced with an SBA lien on the real estate.

To conclude this segment on the combination of seller financing and an SBA loan, it's important to begin with the end in mind. If you decide to seller finance your business, you may have reservations about an SBA loan being part of the deal.

I think you can see that there are a lot of factors about SBA terms and conditions that you should know before you put your business up for sale. Then you need to get clear on what you are and are not willing to do to put a deal together.

The standby requirement for seller notes that are not part of the equity injection, is a good example. Can you imagine finding out about this when you are about to close the deal, as some sellers do? It is much better to decide ahead of time if this is a deal breaker, or what concessions you may require from the buyer.

And not all banks will have the same standby requirements. So by being prepared in advance, you can urge potential buyers to find a lender accordingly.

SBA Update

"On August 1, 2023, SBA implemented policies to expand access to capital for small businesses by modernizing SBA’s signature 7(a) working capital* and 504 fixed asset loan programs. The loan program updates build on industry insights and previous announcements that address long-standing persistent capital access gaps, especially for small-dollar loans and underserved borrowers."

Here is link to the SBA Update referenced above from their memo titled "Business Loan Program Improvements"

Effective June 1, 2025, the Small Business Administration's Standard Operating Procedure (SOP) 50 10 8 has made significant changes to the ways that businesses apply for and receive SBA loans. Live Oak Bank summarizes the changes in their article: "Navigating the SBA's New SOP 50 10 8." Here is a downloadable update of Standard Operating Procedure (SOP) 50 10 8 from the SBA.

In 2026 SOP 50 10 8 has been updated by a procedural notice. Effective March 1, 2026 all owners must be U.S. citizens/nationals with primary residence in the U.S. or its territories. Legal Permanent Residents (green card holders) are no longer eligible to hold any ownership interest in an applicant business.

Conclusion

Seller financing provides a way to sell your business, take control of the process and increase your income resulting from the sale. If you choose this approach, be decisive, learn all you can and carefully hire legal, tax and business advisors.

The better prepared you are, the better position you will be in to let your advisors know how to put a deal together for you.

If selling a note might work in your future plans, you can see the advantages of thinking about this ahead of time. If you reviewed my Business Notes page, you should consider the partial sale of a note as part of your plans. This often works better than the sale of a whole note.

Thank you for reading this article. If you ever have a note for sale, please complete one of my worksheets so I can get to work for you. Whether it's a business note or any other kind, as a note broker NoteSolutions will do the work to maximize the value of your note.

1. According to data from the Census Bureau's 2016 Annual Survey of Entrepreneurs, 99.7% of businesses had fewer than 500 workers. Back to text

2. According to bizfilings.com, “Seller financing is involved in up to 90% of small business sales and more than half of mid-size sales. Back to text

Related Questions

Keep in mind that the answers below apply to seller financing used to sell a business. For commercial real estate the answers may vary. Commercial Real Estate Notes Get The Job Done will help you with commercial real estate notes

Is seller financing a business a good idea?

Most small businesses are sold using some amount of seller financing. This is partly due to the difficulty of obtaining bank financing for these transactions. For the business seller there are tax advantages, interest income and the note is an asset that can be sold. For the buyer seller financing can help to buy a business they wouldn't be able to otherwise, and the chance to negotiate favorable terms. So yes seller financing a business is a good idea.

What are the IRS rules on owner financing?

The IRS rules on owner financing can be found in IRS Publication 537. For tax purposes, seller financing is referred to as an Installment Sale. The term "Installment Sale" comes from Internal Revenue Code(IRC) 453. For property held for more than one year, long-term capital gains rates will apply to installment sale income. Interest income from seller financing is taxed as ordinary income. For more information take a look at What Are The Tax Implications Of Seller Financing?

Who benefits from owner financing?

Both buyers and sellers of businesses benefit from owner financing. The buyer will exert a greater degree of control over the marketing, financing and sales process. Taxes on profit can be paid in the year received which spreads out the taxes over time. To the extent that bank financing is reduced or eliminated, buyer closing costs are reduced. Lender closing costs may include an origination fee, loan packaging fee, tax monitoring fees, flood certification and SBA guarantee fee. Owner financing also gives the buyer much more flexibility to structure favorable terms than dealing with a bank.

References

- Top photo by Mohamed Hassan from Pixabay.

- U.S. Bureau of Labor Statistics provided by FRED, the Federal Reserve Bank of St. Louis.

- IRS Topic No. 705 Installment Sales

- IRS Publication 537

- Exeter 1031 Exchange Services LLC, "Seller Carry Back Notes and 1031 Exchanges."

- Small Business Administration

More Resources For You

Do You Plan To Sell Your Business To Buy Another Business?

Are You Prepared To Sell Your Business?

Conversations About Seller Financing A Business For Sale

Do You Have A Seller Financed Business For Sale? - Part 2

Valuing Your Business For Sale And To Sell Your Business Note